What is the difference between a Credit Report and a Credit Score?

A Credit Report is a listing of all your credit transactions. Who you borrowed money from, when and how much the payments are. It also records if the payments have been made on time or not. Your credit report will also give potential lenders your name, address, date of birth and other demographic information. If you filed bankruptcy in the last 10 years that is listed. Additionally if you have accounts listed with a collection agency those will stay on your report for 7 years. Finally, everyone who has pulled your credit report will be listed. This helps you know who has looked at you report so you can determine if anyone is attempting to commit identity theft. Legally you can only correct inaccurate information on your report. If it’s ugly but accurate, it’s still yours and will be on your credit report.

A Credit Score uses all the information listed on the report to provide a number between 350 and 850. The higher the number the better your score.

If you want a free credit report you must go to annualcreditreport.com. But we are one of the few places on the planet where a live friendly human will help you get your report, explain it to you and help you correct any errors.

How is your credit score developed? What counts?

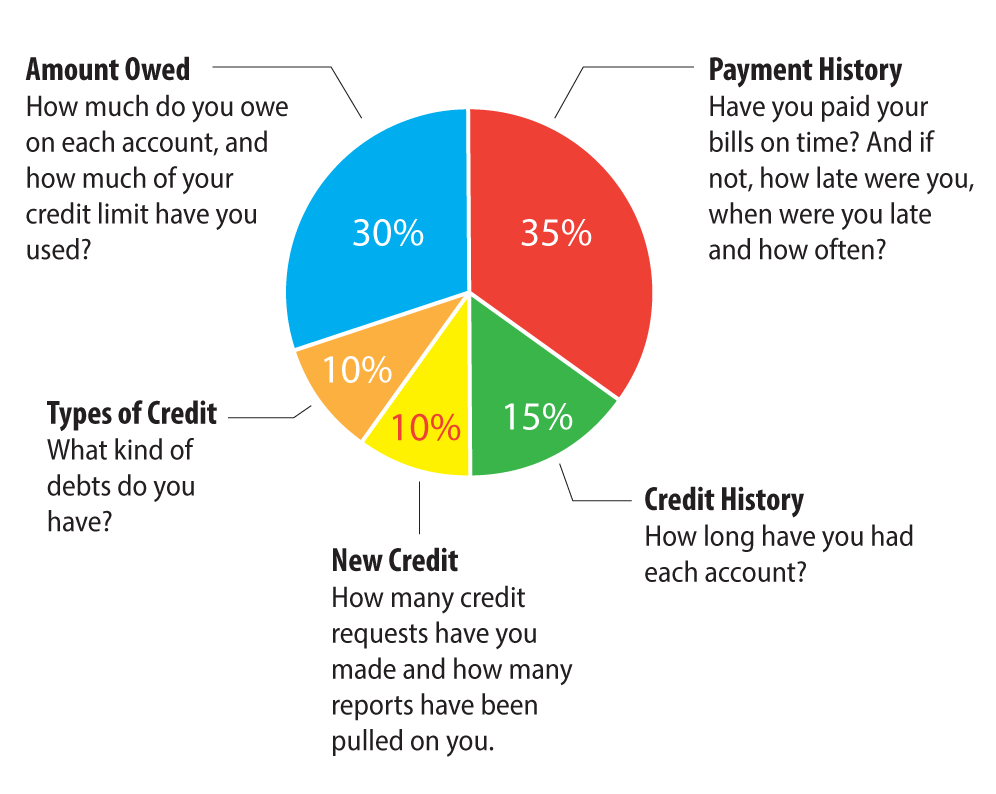

Most important in your score is how you have paid your bills, with emphasis on recent activity. Paying on time is good. Paying them late is bad. Accounts sent to collections are worse. Bankruptcy is the worst. Next most important is the amount you owe. Below you can see how much each factor contributes to the score:

What does NOT count in your credit score?

None of these count: Age, race, job or length of employment, income, education, marital status, whether you’ve been turned down for credit, length of time at your current address, whether you own a home or rent.

What is the average credit score?

| US National | 692 |

| New Mexico | 677 |

| Arizona | 680 |

| Colorado | 695 |

| Utah | 699 |

| Minnesota | 721 – the highest |

| Nevada | 668 – the lowest |

How to maximize your credit score

- Pay your bills on time

- Pay down your debt

- Get your credit report so you know the starting point

- Make sure everything listed is really yours

- Dispute any item that is not yours

- Pay off collection accounts first and quickly as possible

- Get your debt/credit-limit ratio down to 40% or less

- Ask for an increase in credit limits, but don’t use the credit

- Keep the oldest credit cards — the longer you have credit the better

- To have any credit history you must have borrowed money in the last two years

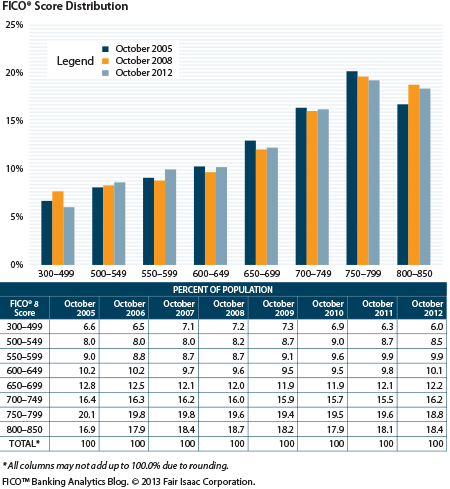

America’s Credit Scores for Individuals (FICO Scores)

FICO, Fair Issac Corporation graph website

What is My Credit Score?

Go to one of these sites to find out:

How do I lock my credit report so no one can look at it?

This is a “Credit Freeze.” This helps protect you from Identity Theft. Even if your identity was stolen, the thief could not open any new accounts under you name.

{kind=link}

{kind=link}

{kind=link}

{kind=link}